[SMM Feature] HRC 2025: Breaking Through the "Ice and Fire," Sounding the Rebound Horn in 2026?

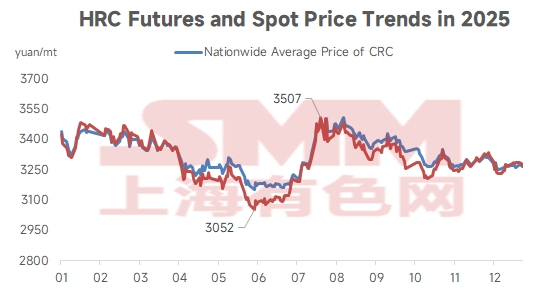

In 2025, HRC prices followed a "concave" trend, with SMM's national average spot price fluctuating between 3153-3506 yuan/mt. The annual average price was 3324.45 yuan/mt, down 8.9% YoY from 3649.38 yuan/mt in 2024. Throughout the year, HRC prices experienced high volatility in Q1, a sharp decline and bottoming out in Q2, a strong rally driven by macro tailwinds such as "anti-involution" in Q3, followed by a retreat from highs, and finally ended with rangebound fluctuations in Q4. The annual average price fluctuation range was relatively narrow, with the price center gradually shifting downward.

- In Q1 [Average Spot Price: 3323-3446 yuan/mt]

In Q1, the HRC market saw a tug-of-war under the macro themes of "overseas policy suppression" and "domestic policy support." Early January's overseas macro headwinds, the US tariff hike in February, and intensified anti-dumping measures against China by various economies, along with the US further announcing additional tariffs in March citing fentanyl, repeatedly dampened market confidence, leading to a weaker futures market and export pressure, which were the main obstacles to price increases. In contrast, domestically, the private enterprise symposium in late February and rumors of macro production cuts around the Two Sessions, as well as reports of coal mine reductions and crude steel production restrictions in mid-March, provided crucial rebound momentum during periods of low market sentiment, demonstrating the supportive role of a "policy bottom." Fundamentally, the market went through a typical seasonal cycle from "inventory buildup during Chinese New Year" to "destocking after the holiday," but the core driver was supply-side adjustments. High supply at the beginning of the year, coupled with seasonally weakening demand, put pressure on prices, while supply contraction in March, combined with resilient demand, facilitated destocking and provided a bottom for the market.

- In Q2 [Average Spot Price: 3153-3365 yuan/mt]

In Q2, the HRC market oscillated and hit bottom under the dual influence of "external policy games" and "internal weak realities." The ups and downs in Sino-US trade relations (tense → easing → optimistic) became the key emotional triggers for short-term price fluctuations, sparking multiple rebounds. However, from the perspective of internal supply and demand, downstream demand for HRC has shown signs of weakness since May and weakened further in June due to seasonal factors. At the same time, with profits remaining good, production gradually rebounded, leading to an inventory turning point at the end of June. The market driver shifted from "policy expectations and supply adjustments" in Q1 to a "weak reality dominance" in Q2. Although external events provided intermittent boosts, they could not offset the pressure brought by strong supply and weak demand, resulting in a stepwise decline in prices.

- In Q3 [Average spot price: 3,176-3,506 yuan/mt]

The HRC market experienced a clear "retreat after rapid rise" trend during the quarter. At the beginning of the quarter, market sentiment was ignited and driven by a series of policy expectations surrounding supply contraction: the "Tangshan sintering production restrictions" and the "Central Finance and Economics Commission's anti-involution" signals in July injected a strong "supply-side reform" imagination into the market; the "Politburo meeting" and "parade production cuts expectations" in August, along with ongoing rumors of "coking coal and coke safety inspections and production restrictions," continuously reinforced the cost support and supply tightening logic, driving prices to rise sharply. However, when policy expectations were fully priced in or even partially failed, the weak actual demand (especially the insufficient "September peak season") and sudden external tariff pressures combined, ultimately driving prices to pull back. This performance also clearly revealed that in the absence of a robust real demand recovery, prices solely driven by policy expectations are unsustainable.

- In Q4 [Average spot price: 3,249-3,352 yuan/mt]

The Q4 market clearly demonstrated the tug-of-war between "weak reality" and "strong expectations." Trade barriers, represented by the EU and US, escalated again in October, and export concerns, which persisted throughout the quarter, peaked in early December due to market rumors about a "steel export licensing system," continuously suppressing market sentiment and export expectations, becoming the main reason for the price pullback. Meanwhile, offsetting the external pressure were frequent domestic market support measures and expectations for production cuts. These included the "Tangshan production restrictions" in late October, the 15th Five-Year Plan, the China-US talks, the "production restriction incidents" and "real estate policy rumors" in late November, as well as document disruptions concerning raw material supply in late December. Whenever weak fundamentals (high inventory, weak demand, export concerns) drove prices to low levels, these optimistic expectations centered on domestic supply-side contraction or macro policies would enter the market to provide support, leading to technical rebounds. However, the extent of these rebounds was ultimately constrained by the weak fundamentals.

Looking ahead to the 2026 HRC market prices, from a policy perspective, attention should be paid to differentiated production control policies using "carbon emissions" as a lever. Simultaneously, the exit of supply capacity from the market is expected to accelerate, with industry leaders likely to be the first to emerge from the industry trough, achieving a bottom reversal. Demand side, against the backdrop of a downturn in the real estate sector, China's macro policies are anticipated to continue strongly supporting the high-quality and precision development of the manufacturing sector. This is expected to drive robust demand growth in industries such as automobiles, home appliances, machinery, shipbuilding, and energy, suggesting HRC demand in 2026 still possesses strong resilience. Furthermore, in recent years, China's steel production has heavily relied on exports for absorption. Affected by anti-dumping measures and export structure adjustments, the decline in HRC export levels in 2026 is also expected to exert some downward pressure on prices. Turning to the supply side, SMM currently estimates that approximately 15.9 million mt of HRC capacity is awaiting commissioning in China in 2026, with the majority planned for H1. The new capacity is primarily concentrated in North China, where 4 production lines are scheduled for commissioning, accounting for 57.86% of the total planned new capacity.

In summary, from a fundamental perspective, given increased supply, moderately resilient domestic demand, and weakening exports, HRC prices in 2026 are forecast to continue fluctuating at the bottom. However, considering the strong expectations for production restriction policy adjustments, the possibility of a price rebound compared to 2025 levels also exists.

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)